High-Frequency Software

Software companies will look like quant funds in the AI era.

As software production time trends toward zero, how will the business of software evolve? The shift from floor stock trading to high-frequency trading offers a rich analogy.

AI will enable software to be delivered at least 10x more efficiently. There is no theoretical speed limit on how fast software business can become. It’s a pure digital domain, not restricted by physical processes like shipping materials. Stock trading similarly had no speed limit—resulting in a competition between automated systems trading 40 million times per day, reacting far faster than humans could.

When a game speeds up by 10x, it’s not the same game anymore. A phase shift occurs—like water turning to vapour: it’s not just hotter—it’s a different thing entirely. The skills that made you successful at the original game often don’t translate to the faster game.

Imagine the traits that made someone successful in “the pit” trading stocks in the New York Stock Exchange in the 1980s. Compare that to the prototypical “quant” building market making algorithms that trade thousands of times per day. These are different universes.

Let’s use this analogy to predict what SaaS may look like after a 10x phase shift.

Agility & Low Conviction Strategies

Hedge funds are not beholden to narrow longterm theses. They aren’t constructed around a singular “mission” that teams spend decades climbing towards. They can take thousands of positions and back out of those positions in a day. When transaction costs approach zero, low conviction strategies like swing trading and high-frequency trading become viable.

Software organizations have historically used strong, pointed narratives to drive alignment around longterm bets. Pivoting an organization of 500 people has an extraordinary cost. But what if a single person can launch 10 landing pages in a day? What if user feedback instantly becomes a live beta feature? What if entering adjacent verticals becomes 99% less costly?

We had high conviction about the problem we were solving at Spellbook, but low conviction on the solution. We launched 100+ landing pages in 3 years in order to find product-market fit. What if we could have done that in 3 weeks?

Software companies of the future will look a lot more like funds: a rapidly evolving portfolio of bets.

Optimized for Latency

High-frequency trading firms go to extreme lengths to optimize for speed. Winning often comes down to one question: how fast can they ingest signals and respond with a “buy” or “sell”? Funds invest in fibre lines and microwave towers. They rent racks next to the US economic data servers so that they can receive inflation data milliseconds sooner than competitors. Lagging behind by 10 milliseconds can mean being left out of the race entirely.

High-frequency software teams will be optimized to respond to the market within hours, not quarters. A new customer request comes in? A prototype will be built by AI immediately. An opportunity emerges in an adjacent market? You’re testing 20 landing pages within 24 hours.

Software teams should be aiming for comically low latency. The lengths that HFT firms have gone to be milliseconds faster would have been considered comically unreasonable to a trader in the 1980s.

If you’re not leaning into “comical speed” territory, you’re probably not thinking fast enough.

Front Running

One way HFT firms take advantage of low latency is front running: algorithms can quickly detect that another party is trying to take a big position. Within milliseconds, the HFT firm can react and make a move first, seizing the opportunity from the competitor.

While originality and first-mover advantages used to be important in SaaS, we are seeing signs of this changing. Front running works. You can see another company starting to do something successful—and replicate it 10x faster with leverage. Ramp executed this playbook well against Brex, even before AI was broadly adopted.

Across AI-capable software companies, front running of competitor functionality is now a constant.

Leverage

When market inefficiencies disappear in seconds—you need leverage to exploit them as fully as possible. You can’t wait to recycle your capital in many loops. Especially when you know your competitors are going to try to front run you as soon as your intent is visible.

Leverage can be a weapon used to capture alpha before competition can react. As speed becomes the advantage, we will see software companies raise larger and larger rounds in order to immediately wipe out competitors. We’re already seeing this happen. In legal AI (Spellbook’s domain) we’re seeing massive rounds—and we’re seeing the herd of AI companies that launched in 2023 get radically culled 2 years later. We hear from a legal AI company looking to get acquired every couple weeks—because they’ve been wiped out by low latency competitors with leverage—and can’t get a foothold.

Edge Funds: Startup + Fund Hybrids

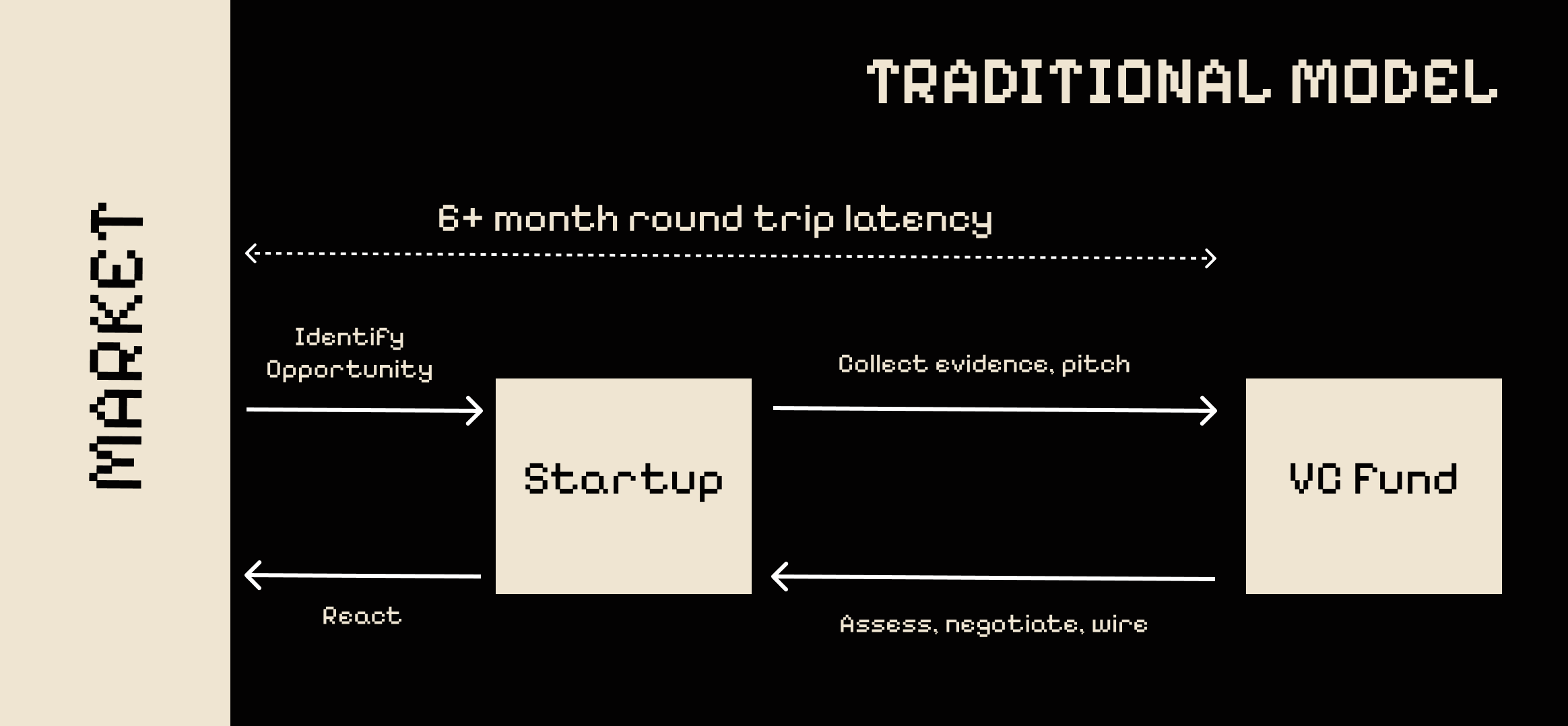

The existing VC model will be at a significant latency disadvantage after 10x acceleration in software. Today, when an opportunity arises in the market, a founder must identify it, collect evidence on it, pitch it, get a term sheet, go through legals, wait for a wire to arrive, hire a team, and execute against it. This takes months.

This wasn’t a bottleneck when it took years to bring software to maturity. But when companies can output mature software in days, and are front running each other in weeks, a 6 month fundraising process becomes a problem.

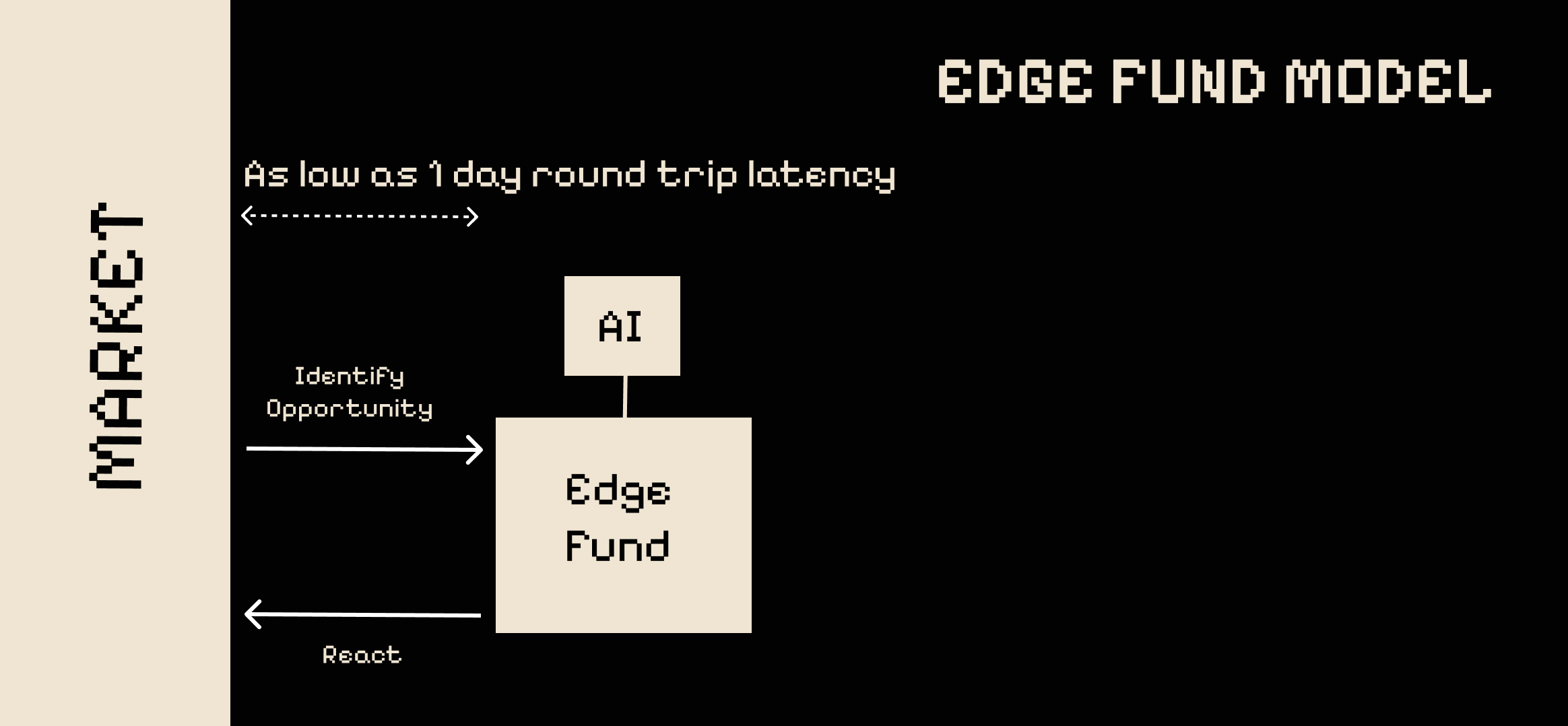

In response, we’ll see new entities bring capital allocation intelligence down from the VC layer to the market’s edge. Let’s call these new entities “edge funds”. They’ll have significant capital earmarked for future unknown opportunities and have a much broader mandate than traditional startups: make money.

Edge funds will have radically low roundtrip latency compared to VC funds. They’ll be like running your trading algorithms next door to the stock exchange. They’ll be able to identify an opportunity in the market and respond to it in hours or even minutes. The traditional “identify an opportunity and then fundraise” model will look comically slow by comparison.

In deep tech, hardware and tough vertically integrated businesses, the traditional VC model will continue to be competitive, because the latency introduced by the fundraising process is fairly low relative to the time to develop a bet.

But in software, I think we’ll see combined startup + fund entities allocating capital much faster, more dynamically and more broadly than we’ve ever seen.

Reinventing AWS for HFS

High-frequency software companies will need a whole new kind of infrastructure to operate: they’ll be managing hundreds of applications and databases—some ephemeral and some long-lived. They’ll have hundreds of homepages and sub-brands, hundreds of advertising accounts managed by AI, and AI sales teams working across many products.

They’ll also need new piping built to feed market signals back to their AI product team: scraping social media, ingesting customer emails, watching competitors, and so on. Their team of AI agents will interpret signals, build feature specs and roll out beta features on their own—monitoring to see what “hits” and what doesn’t.

Maintaining reliability, visibility and security in these environments will be a unique challenge. 10x shifts are phase changes, like water turning to vapour—we won’t just need bigger tools, we’ll need different tools.

There’s a great opportunity for someone to build AWS for the AI era. And many companies will build proprietary software, like quant funds do.

Volatility and Flash Bubbles

High speed automated trading, combined with leverage and front running, can create feedback loops, which result in flash bubbles and flash crashes.

If everyone is front running everyone else, with leverage—it will mean one successful company will quickly become 100 copycat companies—all competing for the same advertising spaces—all competing for the same customers.

Exchanges eventually had to control and regulate activity in order to combat these feedback loops. “Circuit breakers” trigger to halt trading activity when excessive volatility and feedback loops are detected.

It will be a long time before circuit breakers come to SaaS, so we’ll need to be wary of getting sucked into runaway copycat feedback loops. Relying on front running alone is very risky—we still need original ideas.

Order Flow

Order flow, the list of incoming trades on an exchange, is a coveted asset that enables front running. Robinhood originally made money by selling its order flow to hedge funds, rather than charging fees to retail traders. This enabled hedge funds to better front run retail traders.

Who gets to see the “order flow” of opportunities being bet on in software, before anyone else? Although large scale funds may be at a disadvantage in terms of latency, they currently have the clearest view of order flow. For now, they are able to front run, and they can help their portfolio companies front run, by having a broad view of all the bets being made in the market.

Stealth Becomes Cool Again

“Ideas are worth little, execution is everything”: that’s the startup mantra for the past two decades. NDAs are taboo in fundraising. You’ll get laughed if you ask a VC for one.

But what about when execution becomes 10x easier with AI? What about when everyone is trying to front run with superhuman speed? Then ideas start to gain more relative value. A one month lead on executing an idea starts to become meaningful.

I predict we’ll start to see smart founders become more sheepish about sharing their plans. They will pitch less and more selectively. Trust will be more important than ever.

There’s another advantage to startups and VCs merging into a singular edge fund entity: it keeps order flow confidential. LPs may end up investing directly in these entities, without knowledge of how exactly their magic works or about what products will be launched.

Edge funds may operate with extreme privacy, like Renaissance Technology’s Medallion Fund.

Black Box Algorithms: Embracing Illegibility

Complex AI systems, pushed to peak performance are illegible: they are messy, organic and hard to pull apart into components that we can easily make sense of. They’re like a massive matrix of numbers.

If you play chess against a top AI engine, it will make moves that are impossible to reason about. The engine is viewing the world as a large matrix of numbers. Its strategies can’t be explained using simple narratives like: “a great offence is a great defence”.

Similarly, trading firms train blackbox machine learning algorithms which work well, but that can’t always be understood.

Both investors and companies may need to learn to trust AI recommendations even when those recommendations can’t be explained simply in words.

We’ll gain trust in these systems through backtesting.

Backtesting

How do we know when we can allow AI to take over bet making for humans? If the AI has developed a positive track record of making good bets over years—you can extrapolate those returns to the future.

But what about when an AI system is brand new? In trading, firms backtest their automated strategies against historical data to see how they would have done. They feed in historical data and test to see when the model would have bought and sold.

Backtesting is harder to do in software, as our market orders and their results are a lot more complex to model. How would your ideal customer have responded to a hypothetical ad 5 years ago? It’s hard to say.

But elements of SaaS companies are backtest-able. For instance, we ran a backtest recently to see if an AI PM could have come up with the right feature ideas before our own team did, by feeding in customer feedback. In a couple cases, it did beat us.

AI Fracking Kills Bootstrapping

The vast majority of retail traders lose money. Professional traders have too much skill, speed and leverage for retail traders to be able to compete.

There are specialized crevices of the market where a retail investor might have an advantage over Wall Street. Maybe you could learn about a small cap company that doesn’t have enough volume to be interesting to funds.

However, AI algorithms can split their attention in a million directions at once. They can watch all assets, all the time. The better AI gets, the more it can crawl into deep crevices, “fracking” alpha from the market.

Similarly, bootstrapped companies have been able to do well filling needs in small crevices of the market—where the prize is too small for VC-backed companies.

But what about when VC-backed companies have 100 AI tentacles that can reach into these micro-segments?

This is already happening: I spoke with a company the other day that used AI to spin up over one thousand integrations in a month. Previously entire bootstrapped companies existed to service one obscure integration. These crevices in the market are about to be filled by well-capitalized companies, leaving little for bootstrappers.

Winner Takes All

The VC power law will amplify even further. Winners won’t just win one war—they will build a machine that will win hundreds of wars across many products and markets.

Every SaaS company will become a threat to every other SaaS company, as we develop AI tentacles that reach across geographies and verticals. Top SaaS companies will look like top hedge funds.

What Software Companies Should Do

When quants build trading algorithms at Renaissance Technologies, they are not allowed to override the algorithms to make manual trades. They trust their algorithms more than they trust themselves.

Software engineering may take a similar turn over the next 5-10 years, where we must focus on coding the “meta-software” that is ingesting feedback and building products—not on the individual product commits.

We’re not there yet, but there’s a lot companies can do today:

Set up an automated product development workflow that can identify new opportunities and prototype them

Prepare your team to operate with comical speed: many things that would have previously been impossible are now possible. Don’t let your team be traders in the pit rolling their eyes at electronic trading.

Prepare marketing infrastructure to run many product marketing experiments simultaneously—you should be able to stand up and manage landing pages with AI

Start backtesting AI systems (like an AI product manager) against your historical information flow to see where they can beat you, and where they can’t

Welcome to the high frequency software era.